Top Story

Six Developments Selected as Winners of Urban Land Institute’s 2023 Global Awards for Excellence

Read more.

October 31, 2023

Unveiled During Highly Anticipated Fall Meeting in Los Angeles, Emerging Trends in Real Estate lists top markets and industry trends to watch in 2024

WASHINGTON, D.C. (October 31, 2023) – The Urban Land Institute (ULI) and PwC US today released Emerging Trends in Real Estate® 2024, the annual industry-leading report unveiling critical data and trends in the real estate sector. In its 45th edition, the report’s overarching theme is “The Great Reset,” determining that the industry must form new ‘norms’ and can no longer rely on past benchmarks to determine how the market will function in the future.

The report includes proprietary data and insights from more than 2,000 leading real estate industry experts, exploring shifts in the property sector since the pandemic, changing investor sentiment toward climate risks, the emergence of impact investing, and other real estate issues within the United States and Canada.

“It’s clear that the real estate industry is entering a new era of thinking, building and operating. The emergence of hybrid work models, the strength of the retail sector, and the growth of Sun Belt markets underscore the new reality on the ground, specifically in our top cities – Nashville, Phoenix, Dallas/Fort Worth, Atlanta and Austin – to watch in 2024,” said Anita Kramer, senior vice president of ULI’s Center for Real Estate Economics and Capital Markets. “Overall, our data this year shows slightly lower ratings across US markets in terms of development and investment prospects, reflecting a certain degree of caution at the start of the new era. And ratings among top cities are tighter, indicating a sense that there is less difference among market prospects than has been the case. Now, industry professionals are at a turnkey moment that will require both innovation and adaption to shape a resilient real estate landscape for the future.”

“Despite economic headwinds and challenges with obtaining credit, there are opportunities available for high-quality properties that meet the needs of investors and tenants,” said Andrew Alperstein, a leader with PwC’s US real estate practice. “Firms must learn to ride out the current short-term risks and adapt their growth strategy to succeed in this period of higher-for-longer interest rates.”

Emerging Trends in Real Estate® Report’s Top Trends:

Retail outlook is exceeding expectations. Retail tenant demand has skyrocketed over the past 18 months. The United States will close 2023 with roughly 35 million square feet of new retail product across all shopping center types. The industry is coming to realize that the nation will keep shopping for most of its goods and many services in shopping centers indefinitely, even if e-commerce continues to take market share away from in-store retailers – due in the most part to a collective reassessment of the sector than by any dramatic recent shifts in supply and demand dynamics.

Hybrid work is here to stay. The real estate industry has largely accepted that the office sector will not be returning to its pre-pandemic state, as employee work and commuting preferences are standing firm. Office buildings have lost their appeal to investors, with sales transactions down more than twice as much as other major property types. While there is a call for repurposing of high-vacancy office buildings, industry leaders caution that not all can be economically converted, and a better solution may be demolishing them and repurposing the land.

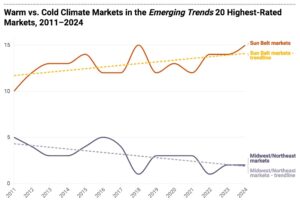

Outlook still sunnier in the Sun Belt. The Sun Belt continues to be an attractive area for households, firms and investors, due to lower regulations and taxes, along with a growing labor force. There is a strong and sustained market correlation between the overall real estate prospect ratings and home builder ratings in this region. Of the top 20 markets for “overall prospects,” 15 of them are located within the Sun Belt. However, escalating risks from climate change could affect the trend of positive investment we’ve seen in this region.

It’s all about the debt. Rapidly rising federal debt could potentially “crowd out” private investments in the industry, leading to slower economic growth and higher interest rates, both of which would create long-term delays on property construction, investments, and returns. Primary debt sources such as originations have fallen, enabling private debt sources to step in where others refuse to lend. Credit has become more expensive and strictly underwritten, leading borrowers to hold onto their existing debt. Despite the lack of credit, some investors are cautiously pursuing deals and lining up to take advantage of undervalued assets. The industry is seeing its highest “buy” rating since 2010, signaling a favorable entry point for acquisitions after a decade of unabating appreciation.

CRE learning to navigate AI. AI advancements are showing promise in the real estate industry, offering capabilities such as enhancing the property search and analysis process, reshaping how investors assess potential investments, improving the customer experience, and streamlining due diligence and fraud detection in real estate transactions. However, despite AI’s tenured use in the industry, many of its capabilities are still largely unknown to our CRE experts, with lack of understanding and AI misinformation being cited as key barriers to adoption.

Adapting for future climate challenges. The number of billion-dollar climate events continues to rise and growing government regulations and ESG mandates, especially in leading CRE markets, means property owners and managers have more reasons than ever to make ESG a priority. A way to achieve more sustainable development is to reposition the development and design process. Not every building will be converted for each of their uses; some assets will simply become obsolete and need to be demolished. Architects and developers are beginning to explore design for disassembly, which could maximize economic value and minimize environmental impacts of destruction and embodied carbon through reuse, repair, remanufacture, and recycling.

Downtowns need to reinvent themselves – again. The future of downtown vitality may hinge on whether the economic forces of agglomeration continue to concentrate high-valued firms and industries into cities. Downtowns face more live/work/play alternative communities in surrounding suburbs, smaller cities and even in their own city neighborhoods that will compete for their economic vitality.

Housing crunch. A key challenge that continues to cause pain is housing affordability. The United States experienced the fastest-ever deterioration in housing affordability over the past three years as housing prices soared during the pandemic, followed by a historic mortgage rate shock that more than doubled mortgage interest rates. After sharp rent escalations last year, rent growth has eased (for now) due to large supply deliveries, but is expected to resume as construction has fallen. One answer has stood out to solve the affordability crisis – build more housing, preferably at all price points.

Emerging Trends in Real Estate® Top Markets

Each year, Emerging Trends in Real Estate® lists top 10 markets to watch. These markets reflect one of the most prevalent trends in this year’s report: the clear interest in development and urban growth in the South. Households are attracted by the warmer weather, more affordable housing, and strong job growth in these mostly Sun Belt markets.

2024 Markets are:

Newly Defined Markets to Watch:

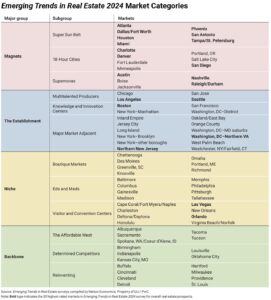

We took the top 80 markets and sectioned them into four main categories, each with three subgroups.

Magnets. Migration destinations for both people and companies, and most are growing more quickly than the U.S. average in terms of both population and jobs.

The Establishment. These markets have long since acted as the nation’s economic engines, including central cities and nearby markets.

Niche. Generally smaller or less economically diverse than the Magnets and Establishment markets but typically have a dominant economic driver that supports stable economic growth.

Backbone. Comprises a wide variety of interesting and enjoyable places to live and work. Many of these metro areas offer select investment development/redevelopment opportunities. There are 18 Backbone markets with more than 30 million residents among them.

Read the full Emerging Trends in Real Estate® 2024 on ULI’s Knowledge Finder platform.

For more information about this year’s report and findings, contact [email protected].

The Urban Land Institute is a non-profit education and research institute supported by its members. Its mission is to shape the future of the built environment for transformative impact in communities worldwide. Established in 1936, the institute has more than 48,000 members worldwide representing all aspects of land use and development disciplines. For more information on ULI, please visit uli.org, or follow us on Twitter, Facebook, LinkedIn, and Instagram.

About PwC

At PwC, our purpose is to build trust in society and solve important problems. We’re a network of firms in 152 countries with over 327,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com.